Rarely a day goes by without news of CBDC progress or the use of tokens to solve critical issues. JP Morgan Chase’s deposit token project is just one example of institutional activity in blockchain and DLT. However, the lack of regulatory clarity is a stumbling block. While every jurisdiction has laws regulating Digital Assets, the lack of cohesion between these laws is creating uncertainty. Anna Carrier, Senior Government and Regulatory Affairs Advisor at Norton Rose Fulbright, says this picture is changing.

“International-level coordination for regulating crypto-assets has only recently gathered pace,” she says, “when earlier this year IOSCO issued for consultation its Policy Recommendations for Crypto and Digital Markets, which aim to promote greater consistency in the approach to regulation and oversight of crypto-asset activities across jurisdictions.”

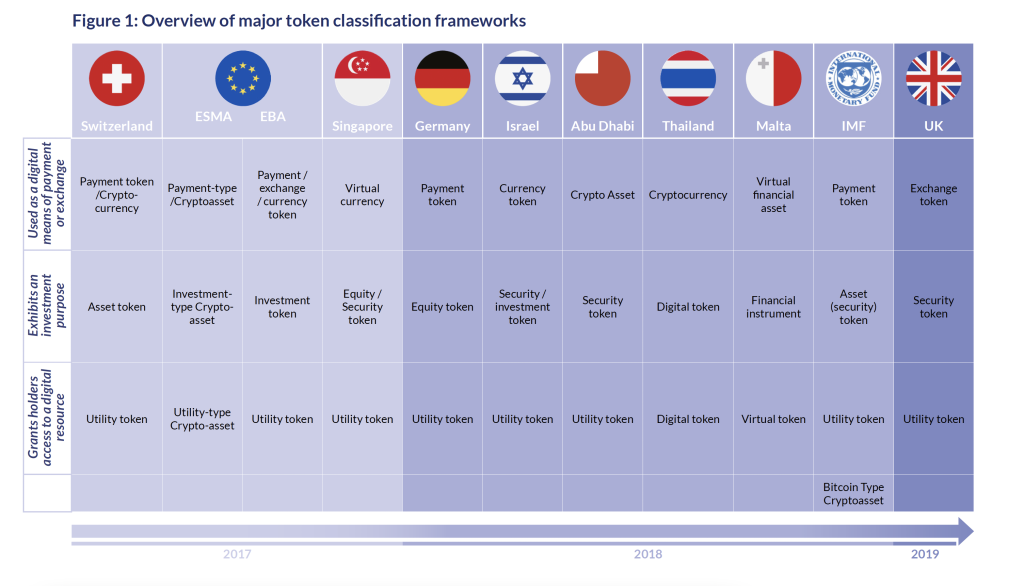

Why is international cohesion taking this long? Examining the current state of affairs in developed markets is a good starting point.

Current regulatory state of the US, EU, and Asia

Lewis McLellan, Editor Digital Monetary Institute at OMFIF, lists a few issues when asked about the state of crypto regulation in the United States. “Uncertainty around the classification of crypto-assets,” he says, “the lack of a clear path to the registration of crypto-businesses, and a lack of clear prudential requirements for them.”

“It is difficult to homogenise the approach of US regulators,” McLellan continues. “The SEC has been criticised (by some of its own commissioners) for regulation by enforcement, suing companies that have made efforts to be compliant but have struggled because of a lack of clarity. The CFTC has generally been less hostile. Various bills in progress on Capitol Hill will determine the approach going forward.”

Carrier echoes these views and is uncertain whether litigation will provide a clear way forward. “Whether the outcome of those cases will lead to regulatory change remains to be seen,” she says. “There are various proposals out, including a recent one for the Crypto Regulation, Protection, Transparency, and Oversight (CRPTO) Act by the New York Attorney General designed to introduce a first comprehensive regulatory framework for the crypto-assets industry in the US. It will be interesting to see further discussions on these proposals and whether or not any of this would be reflected in federal legislation in due course.”

This litigious approach has affected institutional attitudes toward crypto and Digital Assets. Given the American markets’ depth and size, any action there tends to impact assets worldwide.

“Crucially,” McLellan adds, “its regulators have a remarkably broad extrajudicial reach and are happy to exert pressure on businesses headquartered outside the US that serve US customers.”

Carrier opines that with American regulators not leading the charge, the markets might witness a “Brussels effect” where the EU regulatory approach acts as a template moving forward. The EU’s draft legislation on crypto assets, Markets in Crypto Assets Regulation or MiCA, will become law in 2024.

Carrier notes it has already had a significant effect. “We see a lot of those market participants who will seek to become MiCA-authorised crypto-asset service providers (CASPs) already actively preparing for the licensing process,” she says. “We understand that being one of the first to get a MiCA licence is considered by many in the industry as likely to provide a business premium, hence there is a lot of focus on MiCA’s transitional provisions.”

She highlights talk of the potential upgrade of existing MiFID licences to cover crypto activities and transitioning existing regulatory frameworks as a gateway to MiCA as examples of changes occurring. McLellan believes MiCA offers regulators a great opportunity.

“MiCA offers some much-needed clarity on the classification of assets, registration of businesses, and stablecoin prudential obligations,” he says. “It may result in fragmented definitions if other nations do not follow its approach.”

Asia has witnessed high levels of innovation and regulatory support for crypto. The Monetary Authority of Singapore (MAS,) for instance, has commissioned several projects to research the viability of a CBDC and offers incentives for firms looking to set up shop in the city-state. In addition, the authority recently issued rules for stablecoins, defining frameworks for value stability, capital, redemption, and regulatory disclosures.

“Regulation will always inevitably lag behind the current market developments but what makes rulemaking in the area of crypto-assets and DeFi so interesting is how to balance the regulations to make them as future-proof as possible.”

Anna Carrier

Carrier notes this attitude isn’t surprising. “A lot of innovation in crypto-asset markets originates in that region,” she says. “In addition to rules for crypto-asset trading platforms, the regulators in Singapore and Hong Kong are focussing on developments in stablecoin markets and seek to respond to them by creating appropriate regulatory regimes.”

“Japan has taken a cautious approach, implementing strict prudential obligations,” McLellan explains. “This resulted in FTX Japan’s customers receiving their funds much more quickly than in other jurisdictions. VARA, in Dubai, is the framework most frequently cited as providing a model to emulate.”

Taxonomy and standardisation

Given the fragmented nature of crypto regulation worldwide, a taxonomy might offer a way for more harmony between regulations. McLellan thinks a taxonomy could assist jurisdictions that lack regulatory maturity.

“Digital Asset markets are global, and the absence of globally determined regulation means there are jurisdictions with lax or immature regulatory frameworks, which can host crypto businesses that offer their services worldwide,” he says. “This increases the risk inherent in the system and deters large-scale institutional involvement.”

However, Carrier thinks establishing a taxonomy isn’t critical. “Having a standard taxonomy is important but probably not critical,” she says. “Unless we have a single global regulator there will always be differences in terminology.”

“It is important, however,” she continues, “that regulation across jurisdictions remains outcome-based, allowing internationally active market participants to account for such differences. This is not dissimilar to practices existing in traditional finance regulation – where national legislation stems from internationally agreed standards, terminology applied tends to be more consistent, but there will often be differences.”

So is standardisation an impossible goal? “It is probably an overly ambitious goal,” she says. “Ensuring regulatory consistency is arguably more achievable, albeit still challenging. That said, international cooperation between regulators at a global standard-setting level tends to be a good starting point for such regulatory consistency efforts.”

She points to IOSCO’s initiatives at gathering policy recommendations as an example of this.

“Speaking of decentralised finance (DeFi), in September 2023 IOSCO issued for consultation its policy recommendations, covering a broad range of market integrity and investor protection issues for products, services, arrangements, and activities that rely on DeFi solutions,” she says.

“This follows IOSCO’s May 2023 policy recommendations for crypto and Digital Asset markets, addressing key areas of market conduct and regulation.” Carrier points out that while these efforts are a step in the right direction, regulation lags market developments. Given crypto and DeFi’s rapid development pace, regulators find themselves even more behind than usual.

“Digital Asset markets are global, and the absence of globally determined regulation means there are jurisdictions with lax or immature regulatory frameworks, which can host crypto businesses that offer their services worldwide.”

Lewis McLellan

There is plenty of evidence of this gap and McLellan highlights a few. “The US has several problems,” he says. “Uncertainty around the classification of crypto-assets, a lack of a clear path to the registration of crypto-businesses, and a lack of clear prudential requirements for them.

The UK’s update to the FS&M bill places the responsibility for much of the rule formulation in the hands of the FCA. Crypto businesses have found the FCA’s registration process challenging, but I wouldn’t brand this as a problem necessarily.”

Carrier highlights how regulators view market developments differently, even if they’re close to one another. “In terms of the scope of crypto-assets subject to regulation,” she explains, “whilst the definition of a “crypto-asset” is not dissimilar in the EU and the UK, the frameworks differ in terms of exemptions and how to delineate between crypto-assets and other securities.”

Some tokens are also treated differently by UK and EU regulators. “MiCA exempts NFTs from its scope unless they would qualify as crypto-assets,” she says, “whereas the UK proposals suggest that certain activities performed in relation to NFTs may be in scope and, as such, subject to an authorisation requirement.”

Regulation is increasing despite roadblocks

Despite these differences in opinion, regulation is undoubtedly increasing in the crypto sector. Given the relatively nascent nature of this asset class, some fragmentation is inevitable.

“Regulation will always inevitably lag behind the current market developments but what makes rulemaking in the area of crypto-assets and DeFi so interesting is how to balance the regulations to make them as future-proof as possible,” Carrier says. “It is not an easy task but makes cooperation between regulators and industry in the rulemaking process even more important.”

Meanwhile McLellan believes the path to more harmony in regulatory approaches is simple. “Rapid implementation of recommendations from global bodies like BIS, IOSCO, FSB, FATF, etc.,” he says.

Thanks to efforts from global bodies and regulatory action worldwide, institutional market participants can expect a more robust framework for Digital Assets soon.